Every successful retailer understands the importance of retail inventory accounting. However, staying ahead of your competitors and up-to-date on your business requires efficient inventory managerial skills.

Inventory management is the most critical aspect of being a retailer. It is unthinkable to say you understand your retail store’s financial situation. Without knowing the value of your inventory, for instance.

Therefore, in the blog, we will discuss inventory accounting, inventory valuation, and methods used by retailers for inventory accounting. After that, we will discuss how Vencru can help you on this quest.

What Is Inventory Accounting?

Inventory accounting is the procedure for calculating the cost and value of stocks in your inventory. Therefore, it determines the precise value of assets at different stages of production.

What Are The Different Types Of Inventory?

They are 3 different types of inventory accounting:

- Manufactured goods

- Products to be resold

- Products in need of installation

Manufactured goods

Manufactured goods are mainly produced by capital, labor, and raw materials. However, they are also seen as tangible products created by converting material into valuable products.

For example; various food products, electrical equipment, computers, durable medical equipment, transportation equipment, machines, appliances, etc.

Meanwhile, this section is divided into three production stages:

- Firstly, raw goods or raw materials: These are the primary materials used to produce products.

- Secondly, goods-in-process or work-in-progress: In this production stage, products are partly completed – but, not ready to be sold to customers.

- Thirdly, finished goods: These are goods ready to be shipped to the market for sale.

Products to be resold

Have you ever visited a supermarket? Certainly! To clarify, the products you find on their shelves are items tagged as products to be resold. However, this type of inventory is found in retail stores like supermarkets, kiosks, e-commerce businesses (online retail stores), etc. On the other hand, the retailers purchase these products from the wholesalers.

Products in need of installation

These products are used in assembling and installing mechanical and technical parts. For example:

- Cars – Spark plugs, engine parts, tires, etc

- Computers – CPU, hard disks, etc

- Heavy-duty engines, etc

Important Inventory Accounting Key Terms

There are two key inventory accounting terms that retailers should be fully aware of:

- Cost of goods sold (COGS)

- Ending inventory (EI)

Cost of goods sold (COGS)

The cost of goods sold refers to the amount or cost it takes a business to manufacture the products it has sold. Therefore, including everything that went into the production phase – materials, tools, labor employed, for instance.

In calculating COGS, follow the steps below,

- Firstly, figure out the cost of beginning inventory (BI), including the cost associated with labor, raw materials, tools, etc.

- Secondly, add the cost of recently purchased stocks during the accounting period.

- Thirdly, subtract unsold inventory at the end of the accounting period you are calculating.

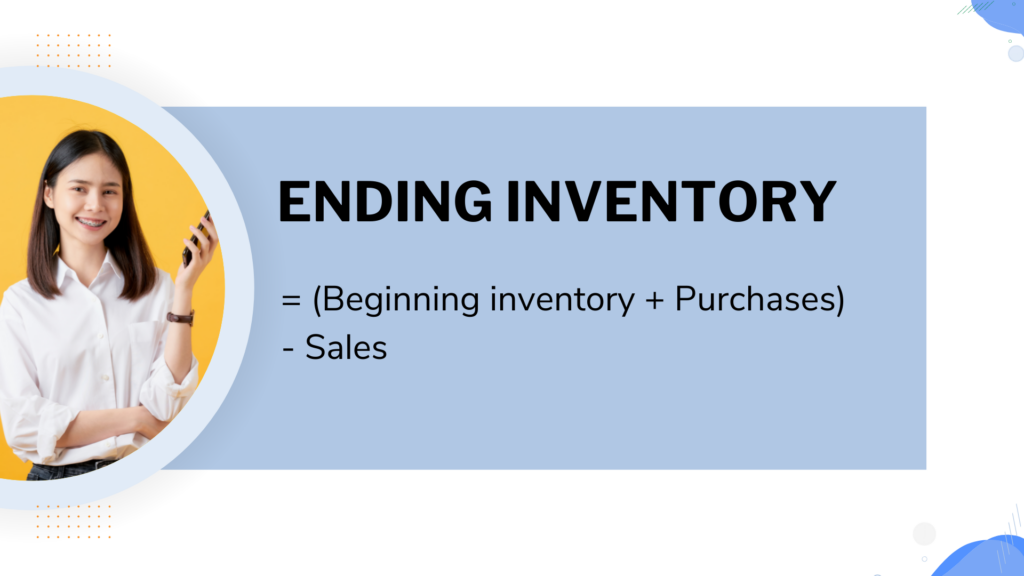

Ending inventory (EI)

At the end of each accounting period, you will notice some unsold inventory. However, this unsold inventory should be included in your financial statements.

To calculate EI, you need:

- Firstly, figure out the value of the beginning inventory

- Secondly, add any current stock bought during the accounting period.

- Thirdly, subtract the total amount of goods sold during the accounting period.

What Are Inventory Valuation Methods, And How Do They Work?

There are three main valuation methods used by retail store owners for inventory accounting:

- First In, First Out (FIFO)

- Last In, First Out (LIFO)

- Weighted average cost

First In, First Out (FIFO)

FIFO inventory valuation method considers inventory purchased first to be sold off first. For example, assuming a retailer sold 200 units of merchandise, but, 150 units were initially purchased by the retailer at $15.00, and 50 units were purchased at $20.00. It can’t assign the $15.00 cost price to every team sold; only 150 units can. However, the remaining 50 items will be given a higher price of $20.00

Some benefits of using the FIFO valuation method are,

- It is easy to understand and trusted

- The oldest merchandise is sold out first. So, you can avoid overstocking or experiencing outdated goods.

- Reduction in waste

Last In, First Out (LIFO)

LIFO is an inventory valuation method for stocks that record recently manufactured items as sold first. So, the last inventory in is the first inventory out.

Using the same example as the FIFO example, the first items to be sold will be the 50 units purchased at $20.00. Subsequently, whatever can be sold from the 150 units will be sold.

Weighted Average Cost (WAC)

This inventory accounting method is also known as the Average cost method. It is based on the weighted average cost of all products procured during a particular accounting period. In addition, Vencru uses the average costing method, which is equally ideal for small businesses. For instance, those that do not track their cost per inventory unit for each purchase.

WAC = Total Cost of Goods for Sale ÷ Total Number of Units Sold

What Is The Importance Of Inventory Valuation In The Retail Industry?

- Sales optimization to ensure a detailed inventory tracking system to ensure your retail store never runs out of stock.

- It helps to reduce the chances of ordering slow-moving merchandise.

- With an organized supply chain, you will reduce the chances of experiencing damaged, outdated, or expired products.

- Most importantly, from the calculation results, you can better understand your profit margins. Therefore, appropriate marketing strategies to boost your retail business or e-commerce business can be set in line.

How Can Vencru Help You?

Vencru is the world’s most trusted solution provider for retail businesses looking to grow their business effectively. Vencru offers you a software solution for your inventory and accounting needs.

For instance, here as such benefits, you stand to gain from using Vencru app as a retailer,

- Up-to-date with stock levels

- Automatically performing inventory accounting

- Preventing double-counting

- Keep track of your debtors

- Track your profit levels

- Avoid wastage of your goods

- Prevent overstocking

- Control employee’s activities

- Manage your client

Final Takeaway

Inventory accounting is a calculated procedure for deciding the cost and value of stocks in your inventory. However, these changes in value can occur for several reasons. For example,

- Obsolescence

- Damages

- Depreciation

- Customer’s change in taste/order

- Increase in demand

- Market supply challenges. etc

Sign up with us now! Get to enjoy the best of our inventory accounting software, customized to your business needs. Stay tuned to our blog and get resources to help you navigate the market. Good luck!